April 30, 2026

First Quarter 2026: Investment Perspective

The Dog That Didn’t Bark

Inspector Gregory: “Is there any other point to which you would wish to draw my attention?”

Holmes: “To the curious incident of the dog in the night-time.”

Inspector Gregory: “The dog did nothing in the night-time.”

Holmes: “That was the curious incident.”

— Arthur Conan Doyle, “The Silver Blaze” (1892)

You probably spend about as much time thinking about the Equity Risk Premium as you do about the Earth’s magnetic field. They are both such primal forces that we tend to take their benevolent presence for granted. Without the magnetosphere, modern life would perish. The unshielded radiation would disrupt satellites, GPS, communications and disable power grids quickly. Gradually, the cosmic radiation would strip the ozone layer—leading to higher surface levels of ultraviolet radiation. This would disrupt our DNA and trigger an explosion of cancers. Simultaneously, plant photosynthesis would be impaired triggering widespread famine. Fortunately, the episodes of geo-magnetic excursions that accompany loss of magnetic shield are rare in the geologic record—maybe as rare as every several hundred thousand years. Not to be alarmist, but scientists who study the magnetic field have become increasingly concerned over the last several decades. The magnetic North Pole has been displacing at increased rates. And two giant areas of decreased flux over South America and Africa have emerged. If you wonder why the tech oligarchs are so interested in space travel, colonies on Mars and building escape bunkers in New Zealand, there’s another theory for your conspiracy quiver.

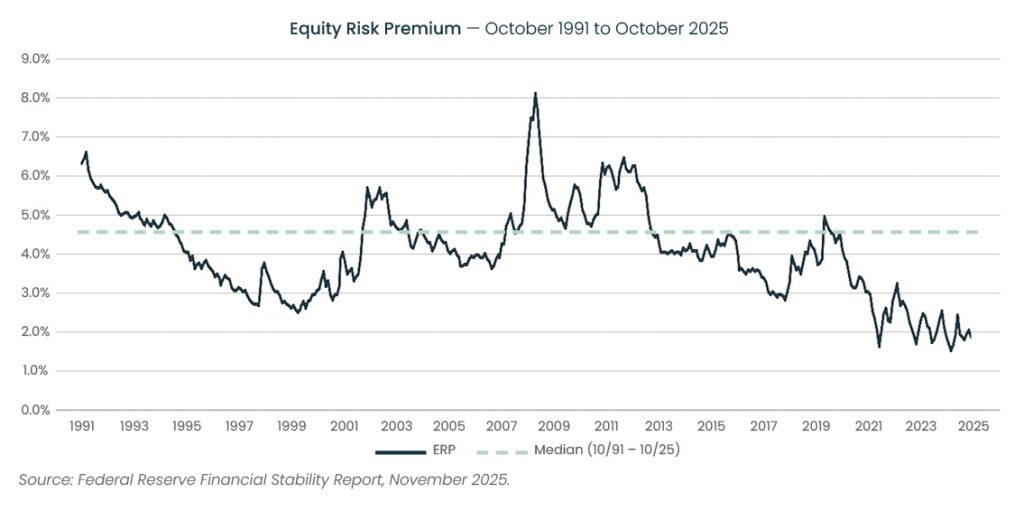

Somewhat closer to home (and reality), I have been pondering that other great anchor of civilization—the Equity Risk Premium (ERP). For a long time, financial economists have perplexed over the ERP. The observed figure for ERP (4-6%) is perhaps 20 times higher than justified by consumption-based asset pricing models with plausible risk aversion. And like the Earth’s magnetic field facilitates life on Earth, so too does the ERP conundrum make financial life so fruitful. Without it, we would have to eke out a living on bond-like returns in all asset classes. Attempts to explain this conundrum could fill a library. My favorite explanation is that the excess return is due to so-called ‘rare events.’ Devaluations, wars, hyperinflations and expropriations have caused catastrophic losses. No matter how low their occurrence, they have great salience for investors. So they are priced into assets at much higher probabilities than their true incidence rates would imply. That salience is the psychological kernel. I just finished Andrew Ross Sorkin’s 1929. It’s a great yarn, and I recommend you read it. But please remember that your interest in Black Tuesday impedes your returns as a shareholder!

In the past quarter, we experienced a rare event. Not just any conflict—but probably the one conflict that has been at the top of the ‘grey swans.’ A black swan comes from a distribution that is unknown. A grey swan is partially predictable but one whose timing and consequences are uncertain. The U.S./ Israel attack onIran’s nuclear capability would have fallen into the same class as the PRC invasion of Taiwan or a buyer’s boycott of the U.S. Treasury market. Worse than the actual conflict has been the closure of the Strait of Hormuz and damage to energy production capacity in the Persian Gulf. And yet, the cost to equity markets has been ‘but a flesh wound.’ The S&P 500 traded down almost 9% from the day before the war to the worst point on March 30. And after the two sides agreed to a cease-fire, even that modest penalty was quickly erased and then some. The S&P 500 Index is now up a little over 3% since before the war.

This is at least the fourth learning episode for risk takers in the last six years. The first was the COVID-19 pandemic. The second was the Silicon Valley Bank almost-bank run. The third was Liberation Day tariff panic. In each case, the really peculiar feature is that the dog did not bark. The market swooned briefly but made a full recovery. If the market were a Pavlovian dog, the operant conditioning would be ‘you’re going to get the treat, no matter what you do.’ Don’t worry about artificial stimuli like bells or lights. Just start salivating, because food is coming. According to the Federal Reserve’s Financial Stability Report, the equity risk premium is now substantially below the 30-year median at about 1.8%.

The Iran War is not an isolated event for the market. It is just one of a series of ‘false alarms.’ And as a result, the market is being slowly conditioned to not price in bad events. Now just like the magnetosphere makes life possible, so too has the ERP made equities so remunerative for so long. The bad news is, if we have reached the limit, equity returns from here will be substantially worse than what we have experienced for 100 years. But why stop here? Perhaps the ERP grinds further into the abyss. Perhaps we gradually extinguish the ERP. In that case, normal equity multiples of forward earnings move to 40x. It’s the stock market equivalent of the singularity. Except in the case of the technological singularity, great things start to happen from that point onwards. For stock market investors, it will be a fantastic ride to get there. But once we get to ZERP (yes, I coined that), it will be the end of equities ‘special role.’

There is an alternate explanation for the missing response to the Iran War rare event. It is perhaps not over. What we are experiencing instead is a sort of phoney war interlude—like WWII between the invasion of Poland and the invasion of France. Exhibit A is that the Strait of Hormuz is—almost one month after the negotiations started—closed to traffic. Exhibit B is that there are no grounds for a negotiated settlement. The Iranians will not now or ever give up uranium enrichment. They will not now or ever give up support for their regional proxies. These two properties are the sine qua non of the Iranian regime. Exhibit C is the Western foreign policy establishment ascribes normal political motives to the Islamic Republic. The Iranian elites may not, in fact, be motivated by money, power and survival like everyone else on the planet. They subscribe to a unique eschatology in which their own destruction might in fact be a glorious victory. I know these are perhaps extreme assertions. But the alternative narrative promoted in Washington that we need only impose more economic pain to walk away with their enriched uranium strikes me as childish. I hope I am wrong, but I am not sure this all resolves blissfully.

DOING THE RIGHT THING FOR THE WRONG REASON

Which leads naturally to a question of how we incorporate views into portfolio construction. There is a pervasive misconception about the role of capital allocation. Since I just suggested that my prior for a negotiated settlement is shy of the market’s forecast, that must mean I have some defined beneficiary for that outcome in our portfolios. Maybe long oil services stocks? This line of thought is natural among security selection strategies. There are two rubs that make the inductive process less applicable to asset allocation. First, individual securities outcomes are typically more bounded. Apple’s new iPhone will either hit a certain volume target or not. Also, these bets are less confounded. Meaning Apple’s iPhone sales will not be affected by a sell off in high yield bonds. Our approach to asset allocation needs to account for the fundamental difference between macro portfolio construction and single stock investing.

This is why we are attracted to assets that have positive convexity across a reasonable array of states of the world, meaning they can benefit from one scenario without getting eviscerated in the polar opposite. Such assets are genuinely rare. Ninety percent of the time assets look linear in the major variables, moving up and down in rough proportion to the same forces already driving the portfolio, and as a result adding them does not meaningfully change its up/down profile. Finding assets that break that pattern is therefore the goal rather than trying to express macro views through positions that will inevitably get muddied by variables outside the original thesis.

U.S. real estate is a current example. REITs were trading at a meaningful discount to historical cap rates, leverage has come down substantially, debt costs have largely reset and the COVID-era emptying of offices has run its course. New supply is trending down, rents appear to have reached a low point and the asset class is deeply under owned among institutions with sentiment near its worst. In a continued status quo REITs were likely to simply tread water. But if the market began to gravitate toward real assets with low obsolescence they could meaningfully outperform equities without catastrophic downside in the base case. That is the convexity we look for, and it played out in the first quarter as the market broadened away from mega cap technology.

As we describe in this note, we’re generally cautious on overall equities on concerns around the achievability of elevated earnings. However, we own a number of positions that are out of favor and we believe can benefit from an expanding risk appetite and improved global economy.

—T. Brad Conger, CFA

Chief Investment Officer

On a quarterly basis, Hirtle & Co. publishes our perspective on the current market. If you would like to be added to our distribution list and receive the full version of our latest Investment Perspective piece, please contact us.

To download a PDF of the excerpt, click here: Investment Perspective 1Q 2026 Excerpt.